Ladies and Gentlemen, THIS is a Budget - Back To Basics

Part Two: No Budget, No Freedom

In 1960 the Greenbay Packers blew a 13-10 lead in the 4th quarter, losing the NFL Championship game to the Philadelphia Eagles.

As the Packers players gathered for day one of the 1961 pre-season training, they fully expected to go over what went wrong and things they could do to improve their performance.

Coach Vince Lombardi had other plans.

When he entered the room with nothing but a football in his hand, he began,

Gentlemen, this is a football.

Sometimes, we just need to start over.

He went back to the very basics. Back to page one in the playbook. They studied the fundamentals of blocking, tackling, passing, receiving, etc.

It wasn’t that they didn’t know these things. They just needed a fresh perspective.

His strategy was that if the basics are nailed down, the goal of winning will take of itself.

That year they won the national championship against the NY Giants 37-0. He went on the win 5 national championships after that and never lost another playoff game.

Ladies and Gentlemen, This is a Budget

This same strategy can be applied to many things we do in life, including how we manage our money.

Sometimes the basics get lost in the living.

First, keep in mind that there is no one way fits all budgeting process.

And, there is a huge array of tools designed to assist you with money management, from simple spreadsheets to sophisticated online budgeting applications and money management software.

These will be covered in the third installment of this series.

The Purpose of a Budget

Freedom.

I know that flies in the face of what many would associate with a budget.

Most see it as restrictive. “If we budget, we won’t be able to have any fun”.

But, what is truly more restrictive?

Having no clue where your money is going and therefore never having enough and going into debt

Allocating $ for specific categories, including debt payoff, with money left at the end of the month and the freedom to use it as you like

Today’s article will focus on how a budget works.

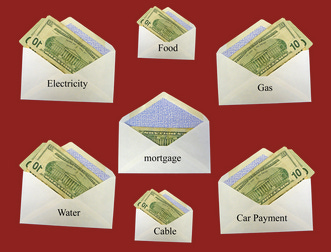

The Three Basic Functions of Budgeting

Assess Spending

Assign Categories

Allocate Funds

Easy Peasy. Right?

The goal is to keep it as simple and easy as possible.

The 3rd Law of building new habits in James Clear’s book, Atomic Habits, is to Make it Easy.

When starting something new, the easier it is, the more likely we will continue to do it. The more we continue to do something, the more habit-forming it becomes.

So, let’s take a brief look at each of these budget fundamentals.

First Basic Function: Assess Spending

Seems like a no-brainer, right? So, why don’t more people do this?

There are a few reasons, but it all boils down to one: Laziness. We simply don’t want to take the time/effort to do it.

Online services like NerdWallet, offer free apps that automate this process by linking to your bank accounts.

They recommend three basic spending categories for monthly expense tracking:

Needs 50%

Wants 30%

Savings 20%

The recommendation is to track spending for at least a month before creating a budget. This allows you to get a handle on exactly where your money is going.

Just to be clear, “tracking” means actually recording spending, not mentally tracking.

This is a must-do if you want to leave the anxiety behind and get off the debt treadmill.

Second Basic Function: Assign Categories

After a month of tracking, you should have a pretty good idea of where your money is going.

Now you can use your findings to create/fund budget categories. This step should be flexible based on your personal needs/wants/savings.

The choices of free or paid budget apps/spreadsheets are almost endless. It all depends on what you want to do and how detailed you want to get.

Again, Nerdwallet has done some research for the best current apps to use. They give category suggestions as well.

Again, this will be covered in more detail in the next article.

Pick which one best suits your needs and get started.

Third Basic Function: Allocate Funds

Experiment with this to find your comfort level.

You can make this as simple or as detailed as you like.

Remember, easy is better for establishing a habit. I started off being extremely detailed and quickly realized it would probably be too tedious for most to stick with it.

You can do broad categories such as -

Home

Household Expenses

Transportation

Charity

Travel

Entertainment

Savings

Emergency Fund

If you want more detail, you can break each broad category down into smaller pieces such as:

Home

Mortgage

Maintenance

Insurance

Taxes

Household Expenses

Groceries

Utilities

Supplies

Transportation

Gas (by vehicle

Oil (by vehicle)

Maintenance (by vehicle)

Charity

Line items (church, non-profits, etc.)

Travel

This could be separate or under Savings

Entertainment

At Home (Streaming services, etc.)

Going out (Restaurants, Movies, Concerts, etc.)

Savings

Travel

Major Purchases

Short Term Goals

Emergency Fund (Self-explanatory)

Debt Payments

Credit Cards, Car Payments, Student Loans, etc.

Just from that example, you can see how detailed things can get. It’s really up to each individual. The key is to not make it so detailed that it becomes cumbersome. If we don’t quickly adjust when that happens, we will quit.

Final Word

A quick note on all this - If you are new to budgeting, you may find that when you account for your spending and channel it into proper categories, you will actually have money left over. When that happens (and hopefully it will), the trick is not to increase your lifestyle expenses to match the increase but to allocate those funds to a category for future use, i.e. travel or savings for a major purchase.

On the flip side, you can look for ways to minimize your financial footprint (tighten the belt) to save even more for things you want to do without compromising your comfort. Things like paying off major debt (mortgage, car loans, etc.) would fit here.

Watch for a post on Financial Footprints soon.

For those looking at retirement on the near horizon and thinking they need a huge nest egg to “maintain” their lifestyle, maybe it’s time to reevaluate that strategy.

A fellow Substacker, Rocco Pendola writes the Never Retire: Living the Semi-Retired Life newsletter.

Rocco has developed a sort of “Reverse Budgeting” process - Starting with the categories, not the income.

Determine how much you need in each category to do what you want to do in life and then create streams of income to fund the categories, which he has dubbed Pots of Money (Keeping it simple).

It’s actually a pretty unique approach that I am inclined to incorporate more into our own budgeting process.

More on that in a future post.

So, that is just a quick overview of basic budgeting.

A simple budget is liberating, not enslaving. Knowing exactly how much money we have set aside for things we need and want brings peace of mind.

In the next article, we’ll delve more into the tool side of budgeting - apps, spreadsheets, etc.

As always, thanks for your support of UnCorked.

Until next time, friends.

Nice breakdown!